by | ARTICLES, ECONOMY, FREEDOM, GOVERNMENT, NEW YORK, OBAMA, POLITICS, TAXES

I have written on this subject before, and now the effects of high taxes and population migration are playing out in a substantial, political way: the decline of about 40% of Congressional seats in the northeast.

According to the Census Bureau, high taxpayers are moving south. It notes that in the 11 states that comprise the Northeast, population grew at a rate of only 15% over the thirty year span from 1983-2013, while the rest of the nation grew at roughly 41%. The key factor is high taxes. The result is a loss of Congressional seats there.

The American Legislative Exchange Council recently did a comprehensive study on House representation in 1950 from Maine to Pennsylvania, and compared it to current House seats. In 1950, there were 141 House members, but today there are only 85. Remember House seats are based on population — so this change is a 40% loss of power.

Need a dramatic comparison? Texas and California combined together now have more House seats than the Northeast conglomerate. For an area that used to be a political powerhouse, it is becoming increasingly marginalized due to excessive taxes and the ensuing population shift.

In 2011, Reuters had a lengthy article detailing how northern residents were fleeing massive state and local tax hikes. I wrote about the impact of high taxes on New York population loss here in 2012. And the NYTimes reported in December 2013 that Florida was soon to pass New York in population.

High taxes are a major factor in this population and political change, and it will be interesting to watch in the next few election cycles. As the report notes above, “This result is one of the most dramatic demographic shifts in American history. This migration is shifting the power center of America right before our very eyes. The movement isn’t random or even about weather or resources. Economic freedom is the magnet and states ignore this force at their own peril.”

by | ARTICLES, CONSTITUTION, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

Thanks to the folks over at CATO, we have a video of the current IRS Commissioner John Koskinen, speaking before the Ways and Means Health Subcommittee early this week. He was being questioned about taxes and Obamacare, and asked about subsidies being repaid.

Chairman Brady said, “The law in that case is that there is not a cap. Subsidies must be repaid. Will you be following the law in that recapture?”

Koskinen replied, “Yes, wherever we can, we follow the law.”

In other words, following the law is a “can”, not a “must”.

With regard to Koskinen’s remarks, Forbes had an interesting observation:

“Numerous Treasury and IRS staffers have told investigators from the House Committee on Oversight and Government Reform that they knew back in 2011 that the Patient Protection and Affordable Care Act didn’t authorize them to issue health-insurance subsidies through Exchanges established by the federal government. But they did so anyway. (And now they’re in court.) The Wall Street Journal‘s Kim Strassel writes about it here.

Given that context, Koskinen’s remark seems like an admission that the IRS sees the law more as a set of guidelines”.

Indeed. I wonder if anyone was to get audited by the IRS, that they could use the phrase “Wherever we can, we follow the law” successfully in their defense.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

According to the Treasury Inspector General for Tax Admininstration (TIGTA), the 2.3% medical device excise tax enacted to help pay for Obamacare is not meeting targets.

The tax went into affect January 1, 2013. The TIGTA report analyzed the returns for the first two quarters (6 months) of 2013, and found that the “excise tax revenue being reported are lower than estimated” for a total of $913.4 million. The IRS expected to have received “excise tax revenue of $1.2 billion for this same period.”

The report also states that the “Joint Committee on Taxation estimated revenues from the medical device excise tax of $20 billion for Fiscal Years 2013 through 2019.”. And yet, in the first six months alone, the estimate amounts are off by 25%. That does not bode well.

Many of the problems originate in the IRS. In fact, the report is aptly named “An Improved Strategy Is Needed to Ensure Accurate Reporting and Payment of the Medical Device Excise Tax”. Some of the key findings:

“The IRS is attempting to develop a compliance strategy to ensure that businesses are compliant with medical device excise tax filing and payment requirements and has taken several measures to advise medical device manufacturers of the new excise tax. However, the IRS cannot identify the population of medical device manufacturers registered with the Food and Drug Administration that are required to file a Form 720 and pay the excise tax.”

“In addition, processing controls do not ensure the accuracy of medical device excise tax figures reported on paper-filed Forms 720. Our analysis of 5,107 Forms 720 processed for the quarters ending March 31 and June 30, 2013, identified discrepancies in the amount of the medical device excise tax and/or taxable sales amount captured from 276 paper‑filed tax returns. TIGTA identified medical device excise tax discrepancies totaling almost $117.8 million when comparing the excise tax amount captured by the IRS from the Form 720 to the excise tax amount TIGTA calculated.”

And the most interesting:

“Finally, the IRS erroneously assessed 219 failure to deposit penalties totaling $706,753 against businesses filing a Form 720 for the quarters ending March 31 and June 30, 2013, which was designated a penalty relief period. The IRS had reversed 133 of the 219 penalty assessments. When TIGTA alerted the IRS of the remaining 86 penalties, IRS management reversed the penalties and issued apology letters to the affected taxpayers.”

The IRS, it seems, was unprepared to handle the collection of excise tax, and furthermore, did not seems to understand basic reporting and penalty relief periods of which it was put in charge.

Think about this: we are now in August of 2014. That means that the second half of 2013 and the first half of 2014 went by before the TIGTA report was released with its findings. If the first 6 months of revenue were found to be about 25% under estimate, it is likely the trend continued for the next full year.

The IRS did agree to the findings of the TIGTA report. However, the summary does not leave one feeling confident that there will be swift resolution now that the problems have been discovered and dissected. Note the ambiguity and qualifiers:

The IRS agreed with our recommendations and plans to consider alternative strategies for identifying noncompliant manufacturers, identify programming changes needed to improve the math verification for paper-filed Forms 720, and implement procedures for corresponding with taxpayers if the changes can be accomplished within budgetary constraints.

Never mind the fact that the Affordable Care Act passed in March 2010 with the excise tax being a key, but controversial, revenue-raiser. The IRS had nearly three years to come up with a) a system to identify companies who owed the tax and b) a system to process the associated forms. And it couldn’t do it.

With the tax being so controversial from the get-go, there have been measures in Congress calling for its repeal because of its impact on the cost of devices and well as jobs in the medical device field.

“The medical device industry has been lobbying hard to get the tax repealed, and there has been movement in Congress. Both the House and the Senate have passed separate pieces of legislation calling for the tax to be repealed, though the Senate vote was on a nonbinding resolution.”

The problem at this point with excise tax repeal is the question of how to make up for even more lost revenue to pay for Obamacare. Taxpayers should be indeed be nervous that the tax collection is showing to be only 75% and we actually have no idea if it improved or worsened at all over the following year because data is not available for it.

The only thing we do know is that we are certain to see a premium rate increases this coming year because the projections have been so off-estimate.

by | ARTICLES, BUSINESS, GOVERNMENT, OBAMA, POLITICS, RETIREMENT, TAXES

A study was released today that showed more than a third of Americans, (36%)a have saved nothing for retirement. That got me thinking about the idea of retirement and the state of retiring in this country.

Everyone thinks they can retire at age 65. It’s an American ideal born in the last century with the rise of unions, the defined benefit plan, and generous pension systems. In reality, especially due to advances in health, medicine, and nutrition, many people have great capability to continue to work and contribute to society and themselves until 80. And they should — because they need to.

There is a crisis of affordability looming. Besides the enormously wealthy, for the most part no average person can afford to retire at 65. It is simply not possible, living a normal lifestyle, for anyone to put enough toward retirement that will enable him to live another 20-30 years. A life span of 85-95 is swiftly becoming the new norm. The only workers today who are the exception to this reality, and have any hope of a lengthy retirement with comfort, are public service employees.

Taxpayers have been long bamboozled into making generous commitments to the retirement systems of public service workers. All over the country, in all levels of federal and state governments, these defined benefit plan pension funds have proven to be vastly untenable. Yet to sustain the plans in their current arrangements and cover the obligations that have already been promised, the rest of society will be duty-bound/compelled to contribute to the retirement of those public service workers via higher taxes. This is turn makes the rest of the populace poorer — because their hard-earned money is being levied to the promised public pensioner, and not for able to be saved for themselves.

The grand scheme is becoming unhinged. One must realize that the more people continue to buy into the idea that they are supposed to “retire at 65”, the more they are suckered into continuing make their retirement years poorer and subsequently make the retirement years of public service employees richer. People see a public service worker being able to retire at that age and they think “I should be able to also do so”. This idea needs to change.

There are two reasons why most people think that such pension programs are still sustainable and normal: their troubles are largely masked because they encompass the larger budget process of federal/state/local governments (and how many people pay attention?) and the costs to keep the programs afloat are borne by all the rest of society — the taxpayers. This arrangement enables a small group of people to be paid a sizeable and continuous pension for until death. It is not out of the ordinary anymore for a person to receive $65K- $100K for the rest of their life. But the actuarial cost to provide that promised benefit is astronomical.

With the lifespan of Americans growing longer, retiring at 65 is no longer viable; the systems are badly strained. And it is certainly not rational for the longevity of Social Security and Medicare either. Yet the steadfast refusal of most of government to overhaul retirement systems or make age and formula adjustments to entitlement programs — in order to maintain this retirement facade — only compounds the problem. (See the latest regarding the annual Social Security report here)

Another one of the biggest detriments of being able to retire at 65 is investment return. Interest rates have been historically low for the last five years and there is a strong likelihood of them staying low for another few. As a result, peoples’ retirement portfolios have lagged in their anticipated growth and goals. The low rates mean less money overall for retirement time, a problem which can be offset by continuing to work and contribute to a retirement fund past the basic age.

Likewise, inflation is not just the issue that everyone thinks it is. The cost of “modern living”, the “keeping up with the Jones”, is a form of lifestyle inflation that adds to the problem. For example, newer models of everything due to technology constantly changing — upgrading TVs, cell phones, etc. are raising the bar for how much pensioners want to comfortably live on and live with.

In sum, with living longer, low rates of return, and the “cost of Jones’s increase”, people must begin to realize that the timespan between 65 – 80 can be, and should be, a healthy and productive time of life. Working, staying active, and continuing to save will be beneficial in the long run. The mindset of older citizens needs to change and they need to understand that they can should aim to be productive until they are 80. At 65 they can certainly slow down, but the concept of retiring and not working anymore at that age is unrealistic and unaffordable.

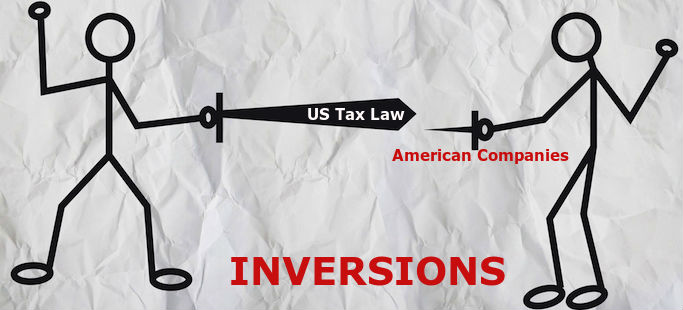

by | ARTICLES, BLOG, BUSINESS, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

When the resident or his advisers talk about inversions these days, they are truly talking about intentional and virulent discrimination of our American companies compared to foreign companies.

In the present environment, U.S. companies are at a severe financial disadvantage compared to foreign companies. Inversions have nothing to do with taxes that the US or foreign companies pay on income they earn within the United States. It all has to do with foreign-earned income, which the United States government lays claim to — and is the only major country to do so. Under U.S. tax law, U.S. companies are forced to pay higher tax rates than other foreign companies on the income they make in foreign countries.

All inversions are, therefore, are a way for U.S. companies to change their HQ from the U.S. to a foreign country, for the sole purpose of allowing themselves the express privilege of being on par with foreign companies and eliminate the severe disadvantage that the U.S. puts on its own businesses!

It is outrageous that the government applies such discrimination. It is outrageous that American companies have to chose to move their headquarters elsewhere simply to survive and compete globally, because they are taxed on their profits in two jurisdictions — both domestic and foreign.

If the government truly abhors the thought of American companies moving their incorporation abroad, then they should drop this tax policy immediately. Make no mistake — every politician who favors this recent, artificial attack on “unpatriotic inversions” shows they are hostile and antagonistic to American companies as well.

For more on what inversions actually are, you can read this earlier article