In a now-deleted Tweet written a week before midterms, President Biden tried to take credit for the Social Security increases that recipients will receive in 2023. The White House twitter account gleefully announced that “Seniors are getting the biggest increase in their Social Security checks in 10 years through President Biden’s leadership.”

The problem is that Social Security increases are based on a formula known as COLA, or cost-of-living adjustment, which measures inflation and the Consumer Price Index. The CPI was up 8.7% in the year-over-year comparison and therefore, seniors will receive an 8.7% adjustment.

It’s worth it to note that this increase is actually the largest since 1981, not just 10 years, because inflation is the worst it has been in four decades. One could argue that indeed it is his leadership (via his atrocious economic policies, mind you) that is the basis for the escalation in prices. But COLA increases and decreases have been tied to the CPI since the 1970s. That’s the law, not the President.

The Committee to Unleash Prosperity recently reminded folks that the prospect of inflation was raised and rejected by a plethora of Nobel prize winning economists as early as last September. As Congress was debating Biden’s $5 Trillion Build Back Better plan, 17 economists signed an open letter urging passage of this atrocious spending bill (coming on top of an extra $3 trillion in spending, mind you).

The letter opened and closed with these two absurd statements: “The American economy appears set for a robust recovery in part due to active government interventions over the past year and a half” and “[the agenda] will ease longer-term inflationary pressures.” At the time of their writing, inflation was at (only) 6% and now we are past 8%. How much more egregious would things be had Congress actually passed this spending behemoth? And even more critically, how is it that 17 prize-winning economists managed to get their economic forecast so wrong?

Readers would be wise to steer clear of the following economists:

George A. Akerlof, Professor, Georgetown University

Sir Angus Deaton, Professor, Princeton University

Peter Diamond, Professor, Massachusetts Institute of Technology

Robert Engle, Professor Emeritus and Co-Director of the Volatility and Risk Institute, New York University

Oliver Hart, Professor, Harvard University

Daniel Kahneman, Professor, Princeton University

Eric S. Maskin, Professor, Harvard University

Daniel McFadden, Professor, University of California, Berkley

Paul Milgrom, Professor, Stanford University

Roger Myerson, Professor, University of Chicago

Edmund S. Phelps, Professor and Director of the Center on Capitalism and Society, Columbia University

Paul Romer, Professor, New York University

William Sharpe, Professor Emeritus, Stanford University

Robert Shiller, Professor, Yale University

Christopher Sims, Professor, Princeton University

Robert Solow, Professor Emeritus, Massachusetts Institute of Technology

Joseph Stiglitz, Professor, Columbia University

It must also be noted that Paul Krugman, another Nobel winner, did not sign the letter but did actively discuss it in his NYTimes column.

These economists had exactly one job: to tell the truth about spending and inflationary policies, namely that increased government spending as a means of intervention will typically result in higher inflation. But they didn’t do that. They would rather tell Congress what it wants to hear, instead of what it needs to hear, and they ought to be ashamed.

As Biden’s presidency continues, it’s become increasingly apparent that he is wholly . unconcerned about the economic wellbeing of our citizens. But what’s less apparent to most people is that he’s taking his cues straight from China’s president, Xi Jinping.

Over the last year, Xi has been targeting wealthy Chinese billionaires, such as Alibaba, for being too successful or not being as aligned with his Communist platform. Using tactics such as increasing regulation or restricting their abilities to do certain things, the value of many successful Chinese companies declined rapidly. Xi claimed that the billionaire businessmen were getting out of control and too powerful, and it was worth it to him to tank their companies to show that communism and being a good citizen was more important than their good fortune or the economic well-being of all individuals.

Biden is doing the same thing. What Xi did unilaterally, Biden needs to get passed in Congress. He is going after the billionaires even if it screws the little guy too. This is why he has consistently pushed to raise corporate rates, implement a global minimum tax, double GILTI taxes, and raise individual rates (which impacts millions of small businesses, by the way). Now this “Billionaire Minimum Income Tax” proposal is just another scheme to punish wealthy Americans to fund absurd government programs. Nevermind that it is purposefully misnamed — it affects more than just billionaires and taxes more than just income — in an effort to sell the idea to legislators and the general public.

Xi took down the economically successful men and women in his country to bolster communism and Joe Biden is following his playbook. He’s happy to punish the wealthy in order to make them more responsible citizens. Biden has repeatedly stated that his goal is a more equitable economy by ensuring corporations and high-income earners pay their fair share (though they are already paying far more than their fair share). Xi would certainly approve.

The concept of an American President (Biden) going after people making a lot of money displays an absolute lack of familiarity with how people get wealthy. As a CPA, I can attest to the fact that the most common way people accumulate massive wealth is either by a huge amount of hard work (creating a successful business) or selling an asset (an invention, real estate, etc).

Many people who file tax returns with large amounts of income, such as selling a business for $10 million, will have a multi-million capital gains amount. It’s not that the higher income earners have some sort of capital gains loophole, but it’s really that the wealthy have done something well to attain the American Dream. And when they do strike it rich through their effort, part of their wealth is treated as a capital gain and it gives those earners a chance to keep a large part of it. Knowing that there is a low capital gains rate is an extra incentive to work hard and be successful.

Many of my clients are wealthy, and I have experienced time and again that they will come to me and ask the question: if they are successful, can they keep the majority of their money?” This is because they know that the government wants to take more from the highest income earners who have proven their success, while at the same time, the government is quite happy to let them lose on their own on their particular endeavor.

Most in the top echelon get there from a one-time income-producing significant event. To punish such success by imposing a massively high capital gains tax only serves to drive a deeper wedge between the have- and have-nots in an attempt to level the economic playing field. Biden would do well to maintain the lower the capital gains rate and restore a sense of trust with those who work hard, contribute to the economy, and attain the American Dream.

When Biden was a candidate, one of his proposals was to raise the capital gains tax (which also applies to dividends) to 39.6%. When I wrote about it at the time, it sounded completely outrageous that any serious candidate for President of the United States would willfully consider implementing such a devastating levy. We had already experienced the negative effects of Obama’s 23.8% tax on capital gains which contributed to the sluggish economic recovery during the Obama administration, and his Vice President now wanted to raise the capital gains rate even higher?

Unfortunately, Biden’s plan has been introduced and may be coming to fruition. This week he indeed announced a new 39.6% capital gains rate (43.4% including the Obamacare add-on), which nearly doubles the current effective rate of 20% (23.8% including the Obamacare add-on).

Yet that’s not the worst of it. Some states with a large concentration of wealthy people and high performing businesses, such as California and New York have recently raised taxes, so taxpayers in those localities will pay much more. The absolute worst area would be NYC; after factoring in local taxes as well as the recent state tax increase, high income earners would face a rate of 57%!

Remember, Economics 1a teaches that when you tax something you get less of it. Taxing investments this way guarantees that investment – economic growth and GDP – will decrease.

Furthermore, this increase is outrageous as a matter of equity and fairness. Taxation of dividends and capital gains is a second tax on the same income – having already been taxed at the corporate level. No other major country double taxes this income. That is the reason dividends and capital gains are taxed at a lower level now – and they should be reduced, not doubled.

Furthermore, raising taxes on capital gains does nothing to raise revenue. Because people have discretion as to whether or when to sell assets, higher capital gains rates invariably lead to lower tax collections! Furthermore, it discourages the sale of less productive assets thereby reducing investment opportunities and economic growth. Even President Obama acknowledged that higher capital gains taxes won’t raise revenue – he was forced to admit that his irrational, hypocritical and wrongheaded rationale was to promote “fairness”!

A massive capital gains tax such as the one proposed by Biden will be inequitable, destructive, and clearly detrimental to our economy and the very people Biden states he is intending to help.

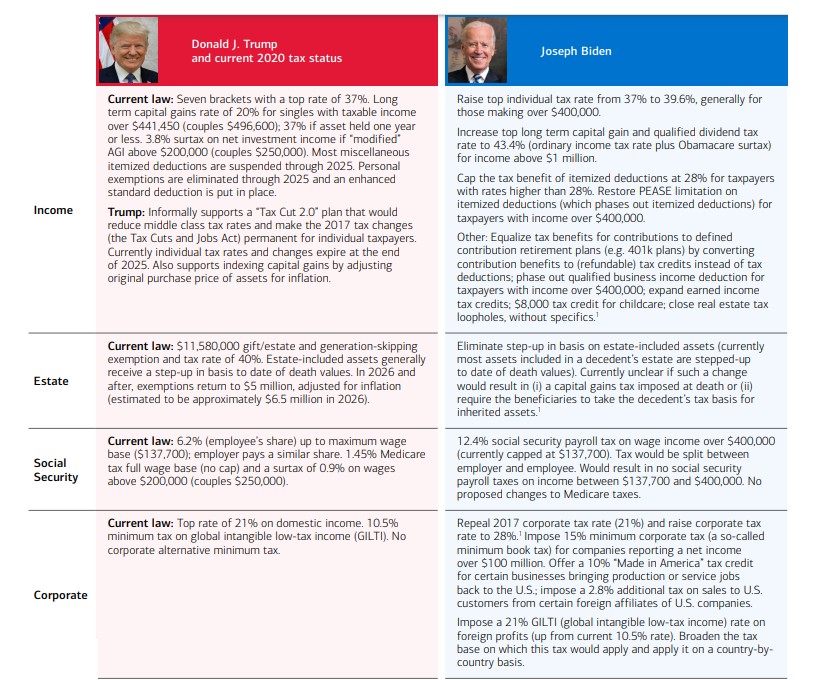

Now that Biden has been elected President, it’s important to take stock of what tax changes are likely to be coming. Merrill Lynch did a good job putting together a side-by-side comparison of current tax law in four areas: income, estate, social security, and corporate, and then possible changes in those areas according to Biden’s campaign tax plans. The summary is below.

It is notable that in just about every instance, there will be a tax increase under Biden’s plans. How this will impact the economy, jobs, wages, and investments remains to be seen.

When I read commentary by people associated with the Club for Growth — known for promoting the rule of law, low taxes, small government, low tariffs, economic growth, etc. — I expect to find analysis consistent with their principles. Therefore, the recent CNS News article on 8/10, “American Manufacturers Come Back, Thanks to Trump,” took me completely by surprise because it was essentially the rantings of someone who is economically ignorant. Ken Blackwell, former elected official in Ohio and current member of the Board of Directors for the Club for Growth advocates for protectionism, pure and simple.

Blackwell praises how Trump instituted “strategic counter-tariffs on bad actors such as China to combat the effects of illegal and abusive trade practices that previously put companies like Whirlpool at an unfair disadvantage.” But this pro-tariff position runs counter to any competent economic analysis. Tariffs clearly and consistently hurt the consumer and taxpayer by driving costs up to everybody in amounts far in excess than any benefits given to those crony beneficiary companies. To call a tariff a “pro-growth economic policy” as Blackwell does is utterly ridiculous, and his entire article reads like a cheap campaign ad.

Tariffs don’t “strengthen” American manufacturers as Blackwell believes; it is cronyism of the highest order. How the Club For Growth — as well as the National Taxpayers Union — can have someone on the board with views that are economically ignorant and destructive to our economy is beyond comprehension.

It’s really sad that Mitt Romney went off the deep end with regard to the commuting of Roger Stone’s sentence. Trump’s timing was definitely politically stupid and over the top. However, presidential pardons and commutations are often self-serving and inexplicable. Although Roger Stone was convicted of a relatively minor infraction of lying about something that was not of major significance, even that conviction was suspect because of clearly stated bias of the lead juror that should have led to a new trial. As such, his commutation was certainly less appalling compared to other pardons sometimes involving really horrific human beings.

Therefore, it is ridiculous that Mitt Romney declared Stone’s commutation was “unprecedented, historic corruption.” This is so absolutely wrong and incompetent that it could only be attributed the most vile case of Trump Derangement Syndrome. It seems that Mitt Romney either doesn’t know his history or is flat-out ignoring the fact that Stone’s commutation is one of a long line of Presidents using their Constitutional powers of pardon to benefit friends. Gerald Ford pardoned Richard Nixon. Richard Nixon pardoned Jimmy Hoffa. Bill Clinton pardoned his brother Roger Clinton and Marc Rich, the “fugitive financier.” Clinton also commuted the sentences of 16 members of FALN, the terrorists responsible for more than 130 bombings spanning several years against the wishes of Congress. Likewise, Obama commuted the sentence of one of the FALN masterminds, Oscar Lopez Rivera, who rejected the original commutation in 1999. Surely these pale in comparison to Roger Stone? As it is, Stone remains a convicted felon because he did not receive a full presidential pardon so he is not completely off the hook.

Romney’s assertions are completely unfounded and shows that his judgement continues to be unreliable. His response was so off the charts that it should make everyone doubt the credibility of anything that he says.

Are we past the tipping point for economic reform? I would argue that Obama’s budgets and spending accelerated the deficits beyond repair. Some people will go back to Reagan and say that the deficit and the debt ballooned during the Reagan Administration and they will blame it on his tax cuts. But what is actually true is that the tax cuts generated a large increase in revenue, and the only reason why he had deficits was that the Democrat-led Congress increased spending even over the increased revenue. The same thing happened with the Bush tax cuts which were very pro-growth; the revenue went up sharply, but spending went up even faster. But at this point the debt was still manageable.

Then you come to Obama. At the beginning of his administration, we had the deep recession -which arguably could have benefited by one year of stimulus. The concept of a stimulus is supposed to be a one-off event. In other words, you engage in big one-time expenditures to get the economy on track and then spending goes back to previous levels as the recovery occurs. The problem is that Obama didn’t put things in for just one year. He did long term things, like food stamps, teacher’s compensation, etc., knowing full well that once put into effect they could not easily be withdrawn. And it was pretty clearly his intent all along, for political reasons, to bake them into the budget. So now when we started to have a recovery, you had ballooning deficits — even with a growing economy. Then by the time Trump was elected, the locked-in recurring spending with its locked-in annual increases made the deficit – and the debt – almost impossible to rein in.

Now we have the pandemic and we have no place to go. There’s no surplus to go to the deficit. Millions of Americans are unexpectedly unemployed, which means they’re not paying into Social Security. At the same time, we see older workers who have lost their jobs choose to draw their benefits as soon as they become eligible. This will speed up the insolvency train. But then Trump did something that was very stupid (though his political motivation is clear). He said that entitlements are off the table. If entitlement reform is off the table at this point, we’re headed to bankruptcy.

We’ve been talking about the coming insolvency of the Social Security and Medicare programs for many, many years now and Congress has done nothing to stave off the inevitable. Couple that with Obama budgets, Trump’s lack of action, and the pandemic, and the deficits are even larger now. Anyone seriously looking at the situation knows that absent a major change to entitlements, the mandated annual increases, both because of cost of living adjustments and demographics, will bankrupt both programs in the next ten to fifteen years. It’s very safe to say that absent major entitlement reform, we’re basically past the tipping point.

House Republicans have put forth a bill that would make some of the tax cuts and changes permanent instead of expiring after a few years. This includes:

The reduction in the individual tax rates

The increased new standard deduction, which went to $12000/individual and $24000 married couples

Special deduction for pass-through business owners

It’s worth noting that the corporate tax reduction was already permanent with last year’s law. Other additional financial parts of this new legislation include:

Allowing employers to join together to offer 401Ks in order to lower costs

Allow 401K users who have an annuity to transfer it tax-free to an IRA

Remove the age ceiling (70½) requiring distributions from IRAs and 401Ks, and continue to contribute up to $6,500/year in an IRA

Create a new universal savings account with a maximum of $2,500/year after tax funds that can used for non-retirement purposes

Allow parents to remove up to $7,500 from a retirement plan without penalty under certain child-related conditions.

Allow 529 college savings accounts to fund various other educational expenses, including apprenticeship programs, home schooling, or child student loan payments.

As if on cue, Democrats rebuke the legislation as being overly beneficial to the wealthy — as if the economic upswing which has helped everyone across-the-board, has not happened. They also chide the bill for adding to the federal deficit, even though Democrats were virtually silent when Obama had very sizeable deficits throughout most his administration. However, putting forth the legislation at this time indicates that Republicans are interested in talking about the strong economy ahead of the midterms elections — which is the smartest thing they can do right now. The GOP missed the chance to make the Bush Tax cuts permanent. They would do well not to make the same mistake twice.