by | ARTICLES, BUSINESS, ECONOMY, ELECTIONS, FREEDOM, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

I have written numerous times in the past few months of the fiscal distress in Puerto Rico. I have discussed how Puerto Rico’s debt crisis is the result of years of government mismanagement, and a major key to getting Puerto Rico back on track is to reduce the size and scope of government.

Now, President Obama is calling on Congress to directly aid Puerto Rico, with a plan that is very near a bailout. I’m reprinting the NYTimes article in full below, so to keep the details about the plan intact. I will write my analysis in a separate article.

_______

“Looking for a way to help debt-ridden Puerto Rico, administration officials on Wednesday proposed an ambitious — if politically perilous — plan that stops short of a direct federal bailout but that its backers hope is sweeping enough to keep the island from becoming America’s Greece.

The plan would create a new territorial bankruptcy regime and impose new fiscal oversight on Puerto Rico, which is mired in the depths of a decade-long recession, running out of cash and struggling to make payments on $72 billion of debt. It represents an urgent bid by President Obama to offer a way forward. But it requires cooperation from a Republican-led Congress bent on imposing spending restraint.

In describing the package on Wednesday, administration officials emphasized that they had exhausted the limits of their own authority to help Puerto Rico, and needed quick action by Congress to avoid a catastrophe.

“Administrative actions cannot solve the crisis,” Jacob J. Lew, the Treasury secretary, said in a joint statement with Jeffrey D. Zients, the National Economic Council director, and Sylvia Mathews Burwell, the health and human services secretary.

“Only Congress has the authority to provide Puerto Rico with the necessary tools to address its near-term challenges and promote long-term growth,” the statement said.

The situation in Puerto Rico “risks turning into a humanitarian crisis as early as this winter,” one senior administration official said, speaking on condition of anonymity because the person was not authorized to speak publicly. Antonio Weiss, Mr. Lew’s counselor, will explain the administration’s plan in Capitol Hill testimony on Thursday.

The Puerto Rican government has already “done a lot” to restore fiscal order, the official added, but “Puerto Rico cannot do it on its own, and the United States government has a responsibility to 3.5 million Americans living in Puerto Rico” to step in with additional help.

The plan was shared late Wednesday with The New York Times and Agencia EFE, a news organization in Puerto Rico. On the same day, the island’s Government Development Bank said it had ended weeks of fruitless negotiations with certain creditors, aimed at persuading them to voluntarily accept lower bond payments. The bank has a bond payment of about $300 million coming due on Dec. 1.

Virtually all of the administration’s proposed plan would have to be refined and approved by Congress. It would create a special territorial bankruptcy regime — something that does not now exist — to give Puerto Rico a place to restructure all of its $72 billion in debt, which it says it cannot hope to repay.

The new regime could ultimately be a new chapter of the bankruptcy code, available only to Puerto Rico and other American territories. A senior administration official said the specifics would be left up to Congress.

In a nod to Republicans in Congress, who have resisted even limited bankruptcy access for Puerto Rico, the administration also proposes to establish an independent body to monitor the island’s fiscal affairs. Its role would be to improve Puerto Rico’s credibility by policing the imposition of structural economic reforms; it would also demand better financial disclosures.

Officials said the oversight body might resemble one that Congress established for the District of Columbia in the 1990s.

At the same time, the package would seek to bring Puerto Rico, where unemployment tops 12 percent and 46 percent of citizens qualify for Medicaid, the federal health program for the poor, into parity with the federal health programs and tax credits available in the states.

The proposal calls for a Medicaid overhaul in Puerto Rico that would expand coverage and access to important services in the short term, and eventually remove a cap that currently applies to the island’s Medicaid program. The effect would be more federal dollars for the Medicaid program in Puerto Rico. Administration officials also said they believed Puerto Rico’s health care facilities needed to be brought up to standards on the mainland.

The administration is also proposing to extend the earned-income tax credit, a refundable credit for the working poor that is payable even to people who earn too little to owe income tax. It is not currently available in Puerto Rico.

Officials said that extending that type of tax credit would help increase the labor participation rate on the island, now a paltry 40 percent, the lowest in the United States and its territories. A fact sheet compiled by the administration said it would provide an “added incentive for formal participation in Puerto Rico’s economy.”

The tax credit, invented by conservative economists, already enjoys some degree of bipartisan backing. Administration officials who detailed the proposal offered no estimate of the cost of extending it to Puerto Rico, nor did they have a cost projection for the Medicaid expansion.

The legislative proposal will be presented on Thursday to the Senate Committee on Energy and Natural Resources, which has jurisdiction over all of America’s territories. It is led by Senator Lisa Murkowski, Republican of Alaska, which was itself a territory until 1959, when it became the 49th state.

Puerto Rico is now barred from seeking any form of relief under Chapter 9, the type of bankruptcy that municipal governments use. The administration’s proposal for a territorial bankruptcy regime represents a bolder approach than the bankruptcy bills that Congress has considered since the island’s debt crisis began.

Federal law allows for cities, counties, special districts and the like to seek bankruptcy protection if their states agree, but the states themselves are excluded. There are concerns that if Puerto Rico gains access to bankruptcy, fiscally troubled states like Illinois might try to follow suit.

Puerto Rico’s creditors have been arguing that the island’s government has been portraying its financial situation as beyond repair, hoping to force the administration and Congress to give it access to Chapter 9 bankruptcy. The recent bankruptcies of distressed cities like Detroit showed them that bondholders can emerge with just pennies on the dollar, and they believe the same thing will happen if Puerto Rico is allowed to declare bankruptcy.

The legislation introduced so far would make bankruptcy relief available only to Puerto Rico’s municipalities and its government enterprises, not to the government itself. Even those limited bills have failed to gain support from Republican lawmakers.

There is some willingness, particularly among top Senate Republicans, to work out a compromise on the bankruptcy issue, according to a person briefed on the matter who was not authorized to speak publicly about it. But the Republican leadership appears willing only to grant Puerto Rico limited access to the bankruptcy courts and only with strings attached, like a federal “control board” to oversee the island’s finances.

Control boards have been used in cases of severe municipal distress to take the power to spend public money out of the hands of elected officials. They do not generally have the powers that bankruptcy judges do to abrogate contracts, such as labor contracts and promises to repay debt.

Both Democrats and Republicans are under pressure to respond to the Puerto Rico crisis. Largely because of the island’s economic problems, Puerto Ricans are flooding the mainland United States, particularly central Florida, and are becoming an increasingly important voting bloc in the 2016 presidential race.

In the hearing, Puerto Rico’s governor, Alejandro García Padilla, will offer his first congressional testimony since his announcement in June that Puerto Rico’s debt had become “unpayable” and he would seek a “negotiated moratorium” with its creditors. His most recent appearance was in 2013, when he accused advocates of statehood of skewing a 2011 plebiscite to make it appear that a majority wanted Puerto Rico to become a state.

“That is a great example of how you can lie with numbers,” he told the same Senate panel at the time.

Another scheduled witness is Pedro Pierluisi, Puerto Rico’s nonvoting member of Congress and the statehood advocate who designed the 2011 voting process that the governor disputed. Mr. Pierluisi introduced the House bill to to give very limited bankruptcy access to Puerto Rico. In September, he testified before the Senate Finance Committee, challenging the governor’s handling of the debt crisis and saying that general-obligation bonds “must be paid — period.” The third witness is to be Mr. Weiss, the special adviser to the Treasury Secretary.”

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

A few days ago, Politico revealed a little gem hidden in the Obama budget:

“In obscure data tables buried deep in its 2016 budget proposal, the Obama administration revealed this week that its student loan program had a $21.8 billion shortfall last year, apparently the largest ever recorded for any government credit program.”

That’s a nearly $22 billion loss — for one program, for one year. Politico described how that the amount is greater than the budgets of the EPA and Interior Department combined, or the NASA program’s budget. But it will be covered entirely by the taxpayer anyway.

How did the federal student loan program rack up such massive debt so quickly? Let’s take a look at Obama’s recent reform efforts and programs to help provide relief to student borrowers.

A 2010 law allowed for repayment caps at 10% of a borrower’s income, though some loan holders were initially ineligible. This was called “Pay As You Earn” (PAYE). There were also some other portions of PAYE that were less talked about by the media, including:

1) If the payment doesn’t cover the accruing interest, the government pays your unpaid accruing interested for up to three years from when you begin paying back your loan under the PAYE program.

2) The balance of your loan can be forgiven after 20 years if you meet certain criteria

3) Your loan can be forgiven after 10 years if you go to work for a public service organization

Obama then expanded the PAYE program in June 2014 via Executive Order. The NYTimes reported that this “extend such relief to an estimated five million people with older loans who are currently ineligible — those who got loans before October 2007 or stopped borrowing by October 2011. But the relief would not be available until December 2015, officials said, given the time needed for the Education Department to propose and put new regulations into effect”.

That recent expansion helped to figure into the staggering re-estimation listed in Obama’s FY 2016 budget. As far as the terms of the costs for just the PAYE program, those have “ballooned from $1.7 billion in 2010 to $3.5 billion in 2013 to an estimated $7.6 billion for 2014.”

What’s more, last June, CNS News reported a huge increase in overall student loan debt by comparing the balanced owed when Obama took office to the balance owed in May 2014:

“Since President Barack Obama took office in January 2009, the cumulative outstanding balance on federal direct student loans has jumped 517.4 percent. The balance owed as of the end of May was $739,641,000,000.00. That is an increase of $619,838,000,000.00 from the balance that was owed as of the end of January 2009, when it was $119,803,000,000.00, according to the Monthly Treasury Statement.”

Comparing that amount to his predecessor, under George W. Bush, “the amount of outstanding loans increased from $67,979,000,000.00 in January of 2001 to $119,803,000,000 in January of 2009, an increase of 76.2%.” That was over 8 years. Obama’s jumped the 517.4% in 5.5 years.

So how does this particularly enormous budget shortfall get resolved? Why, it simply gets tacked directly onto the federal deficit. Since the federal student loan program is considered a credit program, “because of a quirk in the budget process for credit programs, the department can add the $21.8 billion to the deficit automatically, without seeking appropriations or even approval from Congress.” This whopper adds nearly 5% to the deficit itself.

Apparently, this sort of bailout is not entirely uncommon either. According to a report last month on the U.S. Government credit-loan system,

“these unregulated and virtually unsupervised federal credit programs are now the fastest-growing chunk of the United States government, ballooning over the past decade from about $1.3 trillion in outstanding loans to nearly $3.2 trillion today. That’s largely because the financial crisis sparked explosive growth of student loans and Federal Housing Administration mortgage guarantees, which together compose two-thirds.“

The FHA itself has added $75 billion to the deficit in this manner over the last twenty years. Though that is a ridiculous sum itself, it makes the one year, $21.8 billion chunk for the federal student loan program bailout contained in Obama’s FY2016 budget especially egregious and alarming.

Like the ballooning student loan debt, the act of loan forbearance, which is a temporary pause in repayment of your federal student loan, has also seen an upswing. Forbearance can be granted for up to three years. According to the Wall Street Journal, “loan balances in forbearance were about 12.5% of those in repayment in 2006. In 2013, they were 13.3%. Today they are 16%, or $125 billion of the $778 billion in repayment.”

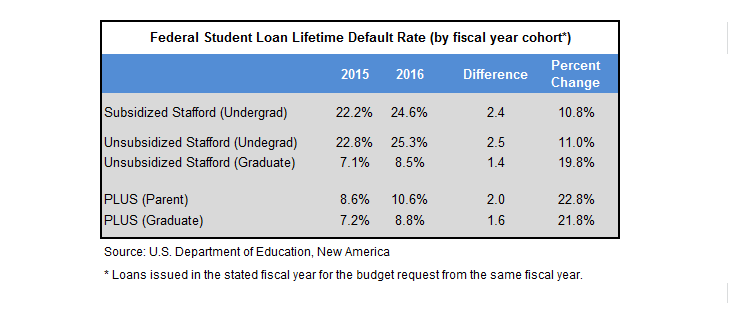

As for defaulting entirely, Forbes recently noted that, “the Department of Education’s budget documents project that 25.3 percent of undergraduate Stafford loans (measured by dollars, not numbers of loans) issued next year will default at some point during the borrower’s repayment term. That is up a full 2.5 percentage points from what the agency projected last year for the previous cohort of loans.” All categories of loans, according to the DoE projection, will see an increase in default.

These figures reinforce a WSJ opinion piece in late December covering the “student debt bomb”. The author, Jason Delisle, director of the Federal Education Budget Project at the New America Foundation, detailed how the current rate of default “now stands at 19.8% of borrowers whose loans have come due — some 7.1 million borrowers with $103 billion in outstanding balances.”

Trying to discern whether or not this $21.8 billion shortfall contained in Obama’s budget is a one-time anomaly or not remains to be seen. The sharp uptick of federal student loan debt and defaults in the past few years would suggest it is not. And there seems to be little incentive just yet to reign in Obama’s repayment reforms, since, at the end of the day, any loss will just be added onto the federal deficit for the taxpayer to pick up the tab — while the Feds continue to tout to young people how much Obama is helping them.

by | ARTICLES, BUSINESS, NEW YORK

How come this bank gets propped up, but others don’t? Crain’s New York has the news here:

The Harlem bank raises $55 million from an investment group that includes titans Goldman Sachs Group Inc and Morgan Stanley; feds had ordered the cash infusion to save the institution.

Carver Federal Savings, the nation’s largest bank founded and run by African-Americans, has staved off possible collapse by raising $55 million in fresh capital.

The investors include Goldman Sachs Group Inc. and Morgan Stanley, which have agreed to invest $15 million each, while Citigroup Inc. and Prudential Financial have agreed to put in $10 million, according to an announcement from Carver’s parent, Carver Bancorp. American Express and three other firms are investing smaller amounts. Chief Executive Deborah Wright, who has led the bank since 1999, will remain at her post.

“I haven’t had a day this good in some time,” said a relieved Ms. Wright, who added she was “terribly grateful” for the financial community’s vote of confidence in her bank. “We have a lot of hard work ahead.”

The Harlem-based bank was ordered by federal regulators earlier this year to raise additional cash as it staggered under a hefty load of delinquent real estate loans. Under Ms. Wright’s leadership, the bank had moved from its traditional business of lending to one- to- four-family homes and into larger commercial real estate projects. That strategy backfired when the real estate market hit the skids and mortgages for low-income borrowers dried up.

Earlier this year, 12.3% of the bank’s loan portfolio was more than 90 days delinquent. The industry average is 4.9%, according to Federal Deposit Insurance Corp. data. In addition, although $74 million of its loans were well overdue, Carver had just $21 million in reserves to cover loan losses.

In February, the U.S. Office of Thrift Supervision ordered Carver to raise additional capital by the end of April or face being seized and sold to another institution—or simply dissolved. The amount Carver raised exceeds the amount demanded by regulators, Ms. Wright said.

Last month, the bank named a new chief financial officer—its fourth in the past three years—and said it hired an recruiter to find a new president and chief operating officer who would oversee lending, retail, marketing and human resources. Ms. Wright said the new executive would allow her to devote the bulk of her time to drumming up new business, adding that Carver will soon step up its marketing.

The Harlem business community galvanized to help rescue Carver, a fixture of the city since 1948. Lloyd Williams, CEO of the Greater Harlem Chamber of Commerce, said a private breakfast was held in late April at Sylvia’s Restaurant in which Ms. Wright and senior Carver officials met with former state Comptroller Carl McCall, former city Comptroller Bill Thompson, U.S. Rep. Charles Rangel and other Harlem business and political leaders to discuss ways to turn around Carver.

“It is exciting, and the community is now stepping up to the plate,” Mr. Williams said shortly after that meeting, “because they have been asked to do so in a meaningful manner.”